using Flux, ForwardDiff, Distributions, Plots, StatsPlots, Random, Zygote, LinearAlgebra, ChainRules, ChainRulesCoreMaximum Likelihood Estimation via Maximum-Likelihood

Simple latent variable model

\[X\sim\mathcal{N}(\mu_h,\sigma_h^2)\] \[Y\sim\mathcal{N}(\exp(\alpha_o\cdot X),\sigma_o^2)\]

struct LatentModel

mu_h

sigma_h

alpha_o

sigma_o

end

Flux.@functor LatentModel

LatentModel() = LatentModel(zeros(1,1),zeros(1,1),ones(1,1),zeros(1,1))

function Base.rand(m::LatentModel, N::Int)

mu_h = m.mu_h[1]

sigma_h = exp(m.sigma_h[1])

alpha_o = m.alpha_o[1]

sigma_o = exp(m.sigma_o[1])

X = randn(N) .* sigma_h .+ mu_h

Y = randn(N) .* sigma_o .+ exp.(alpha_o.*X)

return Y

end

Base.rand(m::LatentModel) = rand(m,1)[1]Specify model for a test case

\[X\sim\mathcal{N}(1,0.25)\] \[Y\sim\mathcal{N}(\exp(0.75\cdot X),0.25)\]

Random.seed!(123)

true_model = LatentModel([1.0], [log(0.5)], [0.75], [log(0.5)])

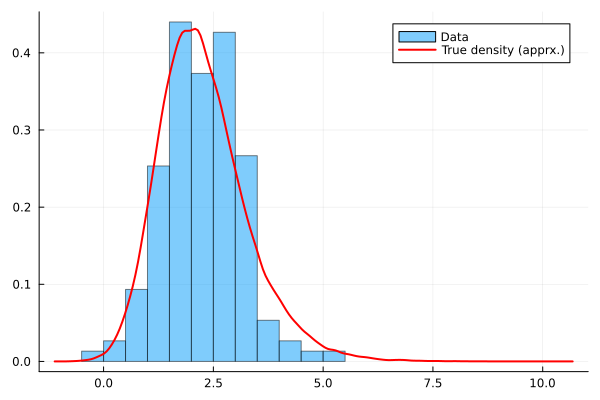

Yfull = rand(true_model,50000) #to plot the density

Y = Yfull[1:150]

histogram(Y,bins=20,normalize=true,alpha=0.5,label="Data",fmt=:png)

density!(Yfull,c=:red,lw=2, label="True density (apprx.)")

True density

\[p_\theta(y)=\int p_\theta(y|x)\frac{p_\theta(x)}{q(x)} q(x)dx\]

Approximated density

\[\hat{p}_\theta(y)=\frac{1}{M}\sum_{j=1}^M p_\theta(y|x_j)\frac{p_\theta(x_j)}{q(x_j)}\]

with \(x_j\) the proposal sample, drawn from \(q(x)\) with sample size \(M\).

Here:

\[q(x)=\mathcal{N}(x|0,4)\]

function particle_ll(m::LatentModel, y, M=1000)

N = length(y)

qdist = Normal(0,2) #q(x))

pdist = Normal(m.mu_h[1],exp(m.sigma_h[1])) #p(x)

ps = map(_->rand(qdist,M), 1:N)

#one particle sample (1:M) per observation (1:N)

odists = map(i->Normal.(exp.(m.alpha_o[1].*ps[i]),exp(m.sigma_o[1])),1:N)

#p(y_i) = 1/M sum_j^M[p(y_i|x_j)p(x_j)/q(x_j)] for i=1:N

ws = map(i->mean(map(od->pdf(od,Y[i]),odists[i]).*pdf.(pdist,ps[i])./pdf.(qdist,ps[i])),1:N)

#1/N sum_i^N log(p(y_i)) (=avearage log-likelihood)

return mean(log.(ws))

endparticle_ll (generic function with 2 methods)m = LatentModel()

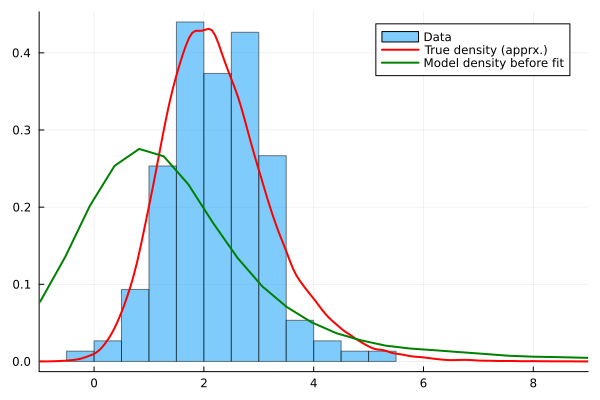

pars, f = Flux.destructure(m)

Yprefit = rand(m,50000)

histogram(Y,bins=20,normalize=true,alpha=0.5,label="Data",xlim=(-1,9),fmt=:png)

density!(Yfull,c=:red,lw=2, label="True density (apprx.)")

density!(Yprefit, c=:green,lw=2, label="Model density before fit")

Random.seed!(123)

for i in 1:250

gg = []

for i in 1:10

g = ForwardDiff.gradient(p->-particle_ll(f(p),Y), pars)

push!(gg,g)

end

grads = mean(gg)

pars.-=0.025.*grads

if i%25 ==0

println(particle_ll(f(pars),Y))

end

end-1.698369499604494

-1.5859668597849523

-1.4757647900932243

-1.3924143414512473

-1.3310941879731057

-1.2977140375800214

-1.2845731201786137

-1.2669498497241503

-1.2622906444844957

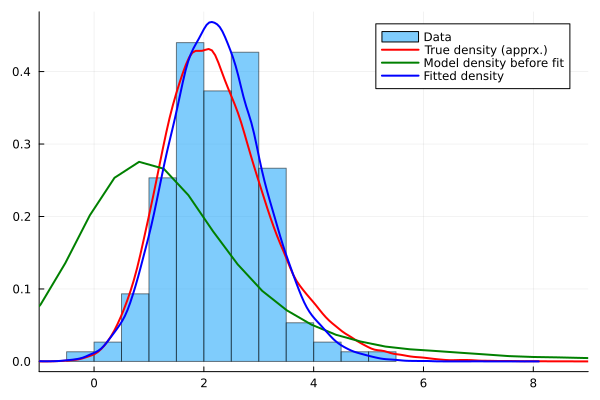

-1.2637100740914606Ypostfit = rand(f(pars),50000)

histogram(Y,bins=20,normalize=true,alpha=0.5,label="Data",xlim=(-1,9),fmt=:png)

density!(Yfull,c=:red,lw=2, label="True density (apprx.)")

density!(Yprefit, c=:green,lw=2, label="Model density before fit")

density!(Ypostfit, c=:blue,lw=2, label="Fitted density")

Stochastic volatility

\[X_t\sim\mathcal{N}(\alpha_h\cdot X_{t-1},\sigma_h^2);\quad -1<\alpha<1\] \[Y_t\sim\mathcal{N}(0,exp(X_t/4)^2)\]

\[X_0=0\] (could also be fitted/trained)

tanh(0.5)0.46211715726000974struct StochasticVolatilityModel

alpha_h

sigma_h

end

Flux.@functor StochasticVolatilityModel

StochasticVolatilityModel() = StochasticVolatilityModel(zeros(1,1).+atanh(0.5),zeros(1,1))

function Base.rand(m::StochasticVolatilityModel, T::Int, X_0=0.0)

alpha_h = tanh(m.alpha_h[1])

sigma_h = exp(m.sigma_h[1])

X = [X_0]

Y = []

for t in 1:T

X_t = randn() * sigma_h + alpha_h*X[end]

Y_t = randn() * exp(X_t/4)

push!(X,X_t)

push!(Y,Y_t)

end

return X[2:end],Y

end

Base.rand(m::StochasticVolatilityModel) = rand(m,1)[1]Specify model for a test case

\[X_t\sim\mathcal{N}(0.9\cdot X_{t-1},0.1^2);\quad -1<\alpha<1\] \[Y_t\sim\mathcal{N}(0,exp(X_t)^2)\]

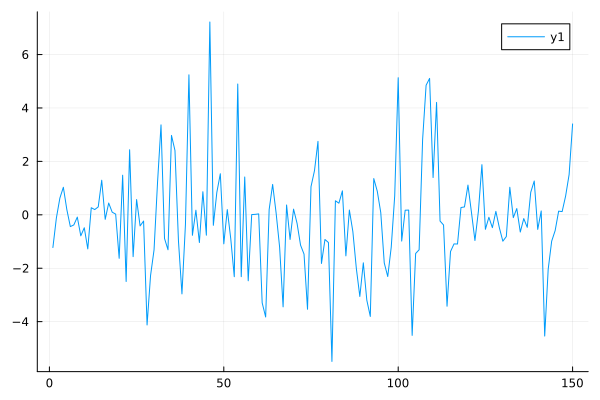

Random.seed!(123)

m = StochasticVolatilityModel(atanh(0.95),0.1)

X,Y = rand(m,150)

plot(Y,fmt=:png)

function particle_filter(m::StochasticVolatilityModel, y, M=1000)

T = length(y)

q0dist = Normal(0,3) #q_0(x)

ps = rand(q0dist,(M,1))

ws = [ones(M)./M]

for t in 1:T

qdists = Normal.(tanh(m.alpha_h[1]).*ps[:,t],exp(m.sigma_h[1]))

ps_t = rand.(qdists)

ps = hcat(ps,ps_t[:,:])

odists = Normal.(0.0,exp.(ps_t./4))

w_t = pdf.(odists,y[t])

w_t = w_t./sum(w_t)

a_t = rand(Categorical(w_t),M)

ps = ps[a_t,:]

end

return ps[:,2:end]

end

function particle_filter_ll(m::StochasticVolatilityModel, y, M=1000)

T = length(y)

q0dist = Normal(0,3) #q_0(x)

ps = rand(q0dist,(M,1))

ws = [ones(M)./M]

for t in 1:T

qdists = Normal.(tanh(m.alpha_h[1]).*ps[:,t],exp(m.sigma_h[1]))

ps_t = rand.(qdists)

ps = hcat(ps,ps_t[:,:])

odists = Normal.(0.0,exp.(ps_t./4))

w_t = pdf.(odists,y[t])

w_t = w_t./sum(w_t)

a_t = rand(Categorical(w_t),M)

ps = ps[a_t,:]

end

return mean(log.(mean(pdf.(Normal.(0.0,exp.(ps[:,2:end]./4)),transpose(y)),dims=1)))

endparticle_filter_ll (generic function with 2 methods)Random.seed!(123)

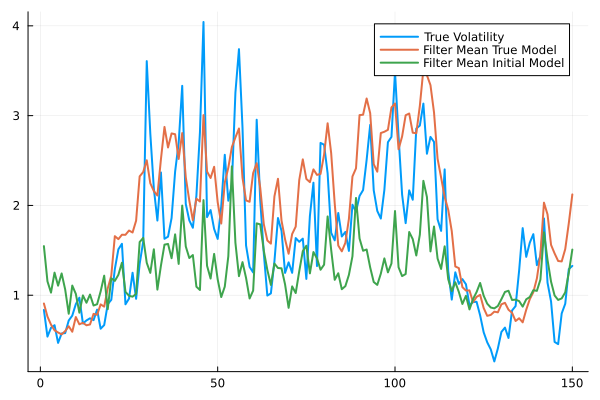

ps_true = particle_filter(m,Y)

filter_mean_true = mean(exp.(ps_true./4),dims=1)[:]

plot(exp.(X./4),label="True Volatility",lw=2,fmt=:png)

plot!(filter_mean_true, label="Filter Mean True Model",lw=2)

ps_initial = particle_filter(StochasticVolatilityModel(),Y)

filter_mean_initial = mean(exp.(ps_initial./4),dims=1)[:]

plot!(filter_mean_initial, label="Filter Mean Initial Model",lw=2)

println(mean((X.-filter_mean_true).^2))2.777623212726044println(mean((X.-filter_mean_initial).^2))4.1040430904059315using FiniteDifferencespars, f = Flux.destructure(StochasticVolatilityModel())([0.5493061443340549, 0.0], Restructure(StochasticVolatilityModel, ..., 2))Random.seed!(123)

for _ in 1:50

gs = FiniteDifferences.grad(central_fdm(15,1),p->-mean([particle_filter_ll(f(p),Y,100) for _ in 1:5]),pars)[1]

pars .-= 0.025.*gs

endRandom.seed!(123)

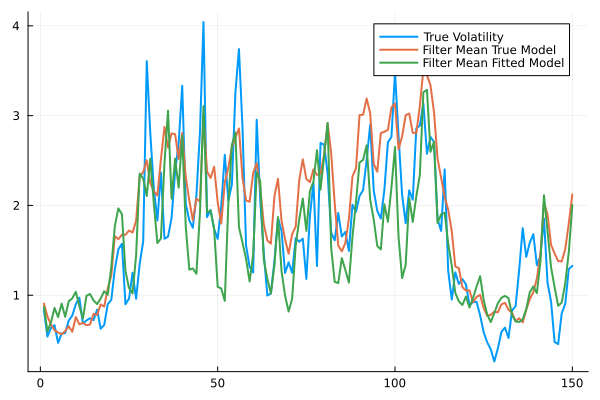

ps = particle_filter(f(pars),Y)

filter_mean_fitted = mean(exp.(ps./4),dims=1)[:]

plot(exp.(X./4),label="True Volatility",lw=2,fmt=:png)

plot!(filter_mean_true, label="Filter Mean True Model",lw=2)

plot!(filter_mean_fitted, label="Filter Mean Fitted Model",lw=2)

println(mean((X.-filter_mean_fitted).^2)) #much better than the initial model3.174579327614477pars #could probably be improved with longer training duration2-element Vector{Float64}:

0.7612290016866907

0.4596682029518793