using Distributions, Plots, StatsPlots, LinearAlgebra, Flux, Zygote, RandomRegression with Time-Varying Coefficients

Random.seed!(123)

b0 = 1 .+cumsum(randn(250) .*0.1)

b1 = -1 .+cumsum(randn(250) .*0.1)

X = rand(250) .*10 .-5

y = b0 .+ b1 .* X .+ randn(250).*0.1

scatter(X,y)

struct TimeVaryingRegression

#Presumes that all coefficients are driven by a random walk

observation_variance

rw_variances

coeff_means_0

coeff_vars_0

end

Flux.@functor TimeVaryingRegression

TimeVaryingRegression(n_coeffs) = TimeVaryingRegression(ones(1,1), ones(n_coeffs), zeros(n_coeffs), ones(n_coeffs))TimeVaryingRegressionfunction kalman_filter(m::TimeVaryingRegression, y, X)

obsvar = exp(m.observation_variance[1])

rw_variances = exp.(m.rw_variances)

coeff_means_0 = m.coeff_means_0

coeff_vars_0 = exp.(m.coeff_vars_0)

return kalman_recursion(y,X,obsvar,rw_variances,coeff_means_0,coeff_vars_0)

end

function kalman_recursion(y, X, obsvar, rw_variances, coeff_means_tm1, coeff_vars_tm1)

coeff_vars_t = coeff_vars_tm1 .+ rw_variances

coeff_means_t = coeff_means_tm1

y_t = y[1]

X_t = X[:,1]

y_t_mean = sum(coeff_means_t .* X_t)

y_t_var = sum(coeff_vars_t .* X_t.^2) + obsvar

coeff_means_t_post = coeff_means_t .+ (coeff_vars_t.*X_t)./y_t_var.*(y_t-y_t_mean)

coeff_vars_t_post = coeff_vars_t .- (coeff_vars_t.*X_t).^2 ./ y_t_var

dist_t = Normal(y_t_mean, sqrt(y_t_var))

if length(y)>1

dists_tp1, coeffs_means_tp1, coeffs_vars_tp1 = kalman_recursion(y[2:end],X[:,2:end],

obsvar, rw_variances,

coeff_means_t_post,

coeff_vars_t_post)

return vcat(dist_t,dists_tp1),

hcat(coeff_means_t_post, coeffs_means_tp1),

hcat(coeff_vars_t_post, coeffs_vars_tp1)

else

return dist_t, coeff_means_t_post, coeff_vars_t_post

end

endkalman_recursion (generic function with 1 method)Xc = Matrix(transpose(hcat(ones(length(X)),X)))

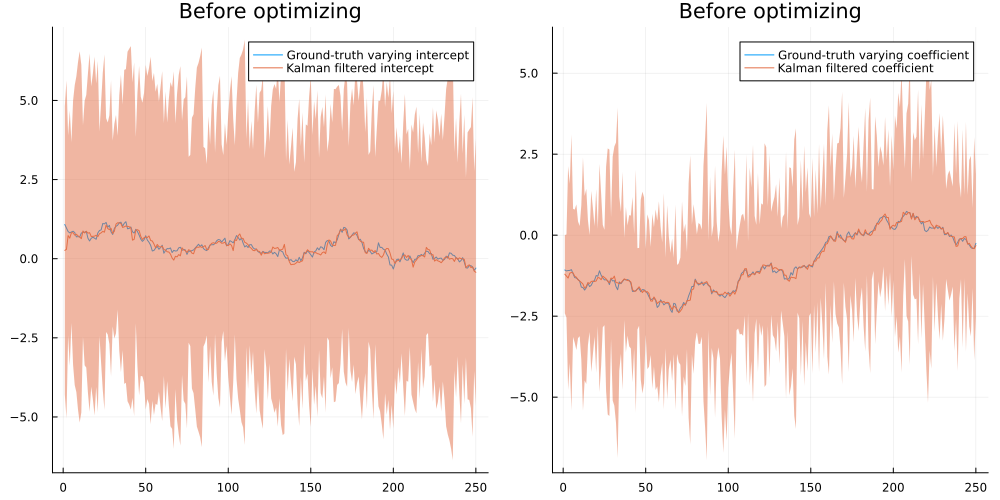

model = TimeVaryingRegression(2)

dists_init, coeff_means_init, coeff_vars_init = kalman_filter(model,y,Xc)

p1 = plot(b0, label="Ground-truth varying intercept")

plot!(p1,coeff_means_init[1,:],ribbon= 2 .*sqrt.(coeff_vars_init[1,:]),label="Kalman filtered intercept")

p2 = plot(b1, label="Ground-truth varying coefficient")

plot!(p2,coeff_means_init[2,:],ribbon= 2 .*sqrt.(coeff_vars_init[2,:]),label="Kalman filtered coefficient")

plot(p1,p2,size=(1000,500),fmt=:png,title="Before optimizing")

params = Flux.params(model)

opt = ADAM(0.01)

for i in 1:750

grads = Zygote.gradient(()->-mean(logpdf.(kalman_filter(model,y,Xc)[1],y)),params)

Flux.Optimise.update!(opt,params,grads)

if i%75==0

println(mean(logpdf.(kalman_filter(model,y,Xc)[1],y)))

end

end-2.288221451538594

-1.9186016853033478

-1.5566676823511598

-1.2105732966002392

-0.8960431987239883

-0.6384258159294061

-0.46535619001464007

-0.3817636167174806

-0.3554198660243631

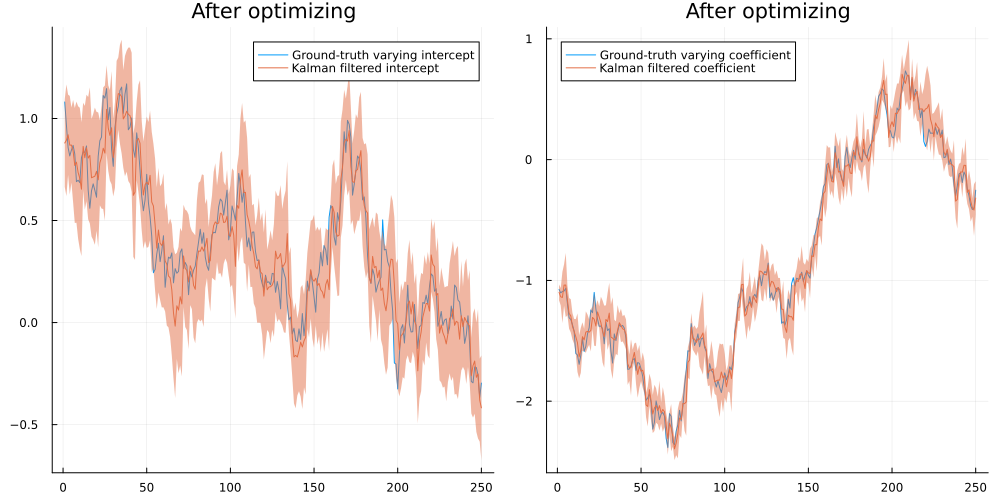

-0.349155862641175dists_opt, coeff_means_opt, coeff_vars_opt = kalman_filter(model,y,Xc)

p1 = plot(b0, label="Ground-truth varying intercept")

plot!(p1,coeff_means_opt[1,:],ribbon= 2 .*sqrt.(coeff_vars_opt[1,:]),label="Kalman filtered intercept")

p2 = plot(b1, label="Ground-truth varying coefficient")

plot!(p2,coeff_means_opt[2,:],ribbon= 2 .*sqrt.(coeff_vars_opt[2,:]),label="Kalman filtered coefficient")

plot(p1,p2,size=(1000,500),fmt=:png,title="After optimizing")

Actual dataset

http://archive.ics.uci.edu/ml/datasets/Bike+Sharing+Dataset

using CSV, DataFramesdf = CSV.File("Bike-Sharing-Dataset/day.csv") |> DataFrame

dates = df[!,:dteday]

X_bikes = Float64.(transpose(Matrix(df)[:,3:end-3]))

feature_names = names(df)[3:end-3]

y_bikes = Float64.(Matrix(df)[:,end])731-element Vector{Float64}:

985.0

801.0

1349.0

1562.0

1600.0

1606.0

1510.0

959.0

822.0

1321.0

1263.0

1162.0

1406.0

⋮

4128.0

3623.0

1749.0

1787.0

920.0

1013.0

441.0

2114.0

3095.0

1341.0

1796.0

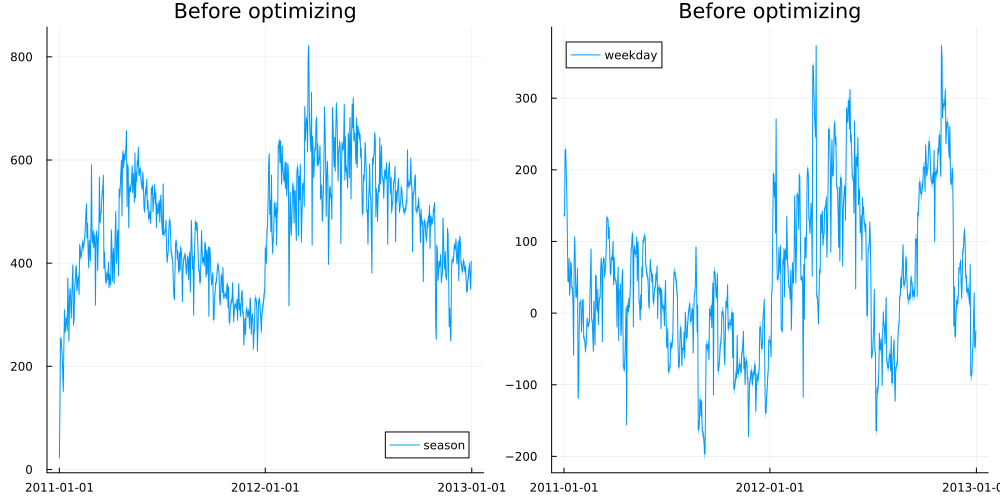

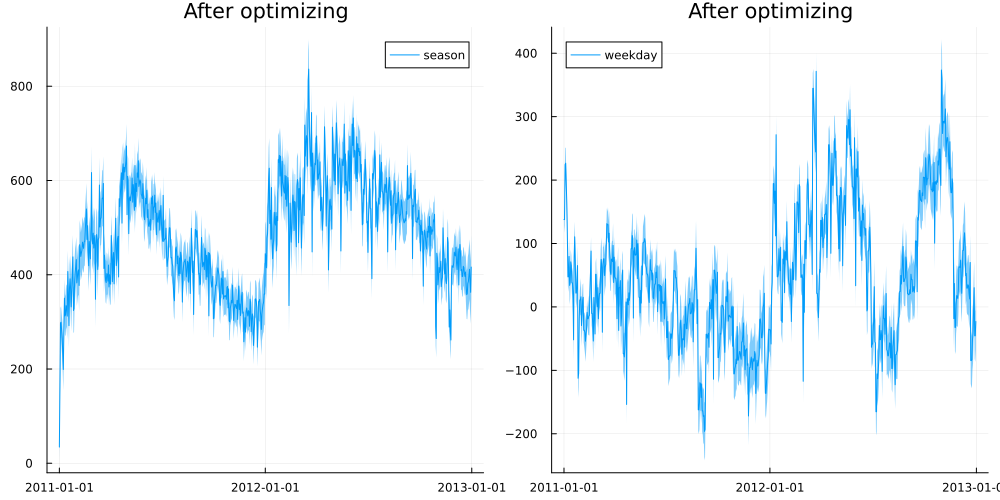

2729.0model_bikes = TimeVaryingRegression(size(X_bikes,1))

dists_init, coeff_means_init, coeff_vars_init = kalman_filter(model_bikes,y_bikes,X_bikes)

p1 = plot(dates,coeff_means_init[1,:],ribbon= 2 .*sqrt.(coeff_vars_init[1,:]),label=feature_names[1])

p2 = plot(dates,coeff_means_init[5,:],ribbon= 2 .*sqrt.(coeff_vars_init[5,:]),label=feature_names[5])

plot(p1,p2,size=(1000,500),fmt=:png,title="Before optimizing")

params = Flux.params(model_bikes)

opt = ADAM(0.01)

for i in 1:1000

grads = Zygote.gradient(()->-mean(logpdf.(kalman_filter(model_bikes,y_bikes,X_bikes)[1],y_bikes)),params)

Flux.Optimise.update!(opt,params,grads)

if i%100==0

println(mean(logpdf.(kalman_filter(model_bikes,y_bikes,X_bikes)[1],y_bikes)))

end

end-238.7240357728576

-136.91278037253636

-91.21076715361971

-66.48041590921156

-51.461287011112326

-41.59519891957266

-34.73519418523346

-29.75560682594894

-26.016930691810636

-23.132324011570695dists_opt, coeff_means_opt, coeff_vars_opt = kalman_filter(model_bikes,y_bikes,X_bikes)

p1 = plot(dates,coeff_means_opt[1,:],ribbon= 2 .*sqrt.(coeff_vars_opt[1,:]),label=feature_names[1])

p2 = plot(dates,coeff_means_opt[5,:],ribbon= 2 .*sqrt.(coeff_vars_opt[5,:]),label=feature_names[5])

plot(p1,p2,size=(1000,500),fmt=:png,title="After optimizing")

function kalman_smoother(m::TimeVaryingRegression, coeff_means_post, coeff_vars_post)

coeff_means_TT = coeff_means_post[:,end]

coeff_vars_TT = coeff_vars_post[:,end]

rw_variances = exp.(m.rw_variances)

coeff_means_tT, coeff_vars_tT = kalman_smoothing_recs(coeff_means_post[:,1:end-1], coeff_vars_post[:,1:end-1],rw_variances,coeff_means_TT,coeff_vars_TT)

return hcat(coeff_means_tT, coeff_means_TT), hcat(coeff_vars_tT, coeff_vars_TT)

end

function kalman_smoothing_recs(coeff_means_post, coeff_vars_post, rw_variances, coeff_means_tt, coeff_vars_tt)

coeff_m_tm1 = coeff_means_post[:,end]

coeff_v_tm1 = coeff_vars_post[:,end]

coeff_m_t = coeff_m_tm1

coeff_v_t = coeff_v_tm1 .+ rw_variances

coeff_m_tT = coeff_m_tm1 .+ coeff_v_tm1./coeff_v_t.*(coeff_means_tt.-coeff_m_t)

coeff_v_tT = coeff_v_tm1 .+ (coeff_v_tm1./coeff_v_t).^2 .* (coeff_vars_tt .- coeff_v_t)

if size(coeff_means_post,2)>1

coeff_means_tT, coeff_vars_tT = kalman_smoothing_recs(coeff_means_post[:,1:end-1], coeff_vars_post[:,1:end-1],rw_variances, coeff_m_tT, coeff_v_tT)

return hcat(coeff_means_tT, coeff_m_tT),hcat(coeff_vars_tT, coeff_v_tT)

else

return coeff_m_tT, coeff_v_tT

end

endkalman_smoothing_recs (generic function with 1 method)coeff_m_s, coeff_v_s = kalman_smoother(model_bikes, coeff_means_opt, coeff_vars_opt)

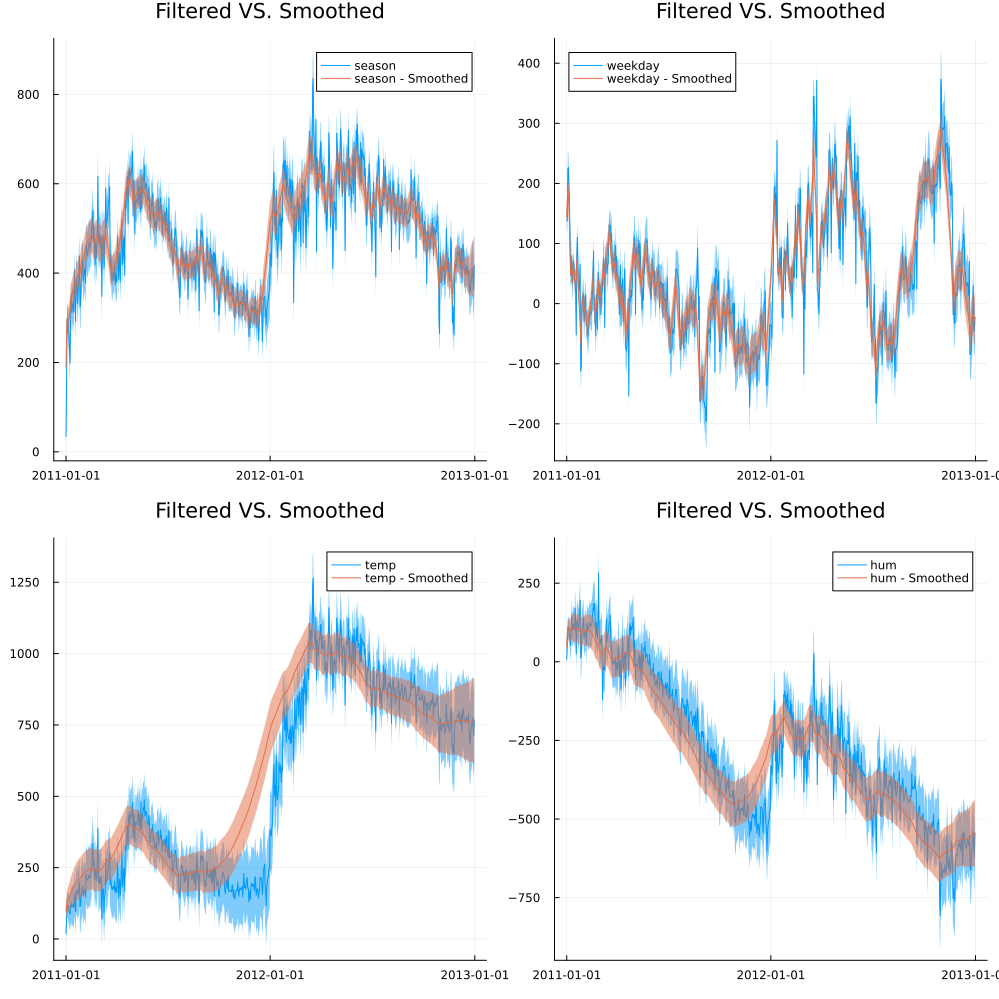

f1 = 1

f2 = 5

f3 = 8

f4 = 10

p1 = plot(dates,coeff_means_opt[f1,:],ribbon= 2 .*sqrt.(coeff_vars_opt[f1,:]),label=feature_names[f1])

plot!(p1,dates,coeff_m_s[f1,:],ribbon= 2 .*sqrt.(coeff_v_s[f1,:]),label=feature_names[f1]*" - Smoothed")

p2 = plot(dates,coeff_means_opt[f2,:],ribbon= 2 .*sqrt.(coeff_vars_opt[f2,:]),label=feature_names[f2])

plot!(p2,dates,coeff_m_s[f2,:],ribbon= 2 .*sqrt.(coeff_v_s[f2,:]),label=feature_names[f2]*" - Smoothed")

p3 = plot(dates,coeff_means_opt[f3,:],ribbon= 2 .*sqrt.(coeff_vars_opt[f3,:]),label=feature_names[f3])

plot!(p3,dates,coeff_m_s[f3,:],ribbon= 2 .*sqrt.(coeff_v_s[f3,:]),label=feature_names[f3]*" - Smoothed")

p4 = plot(dates,coeff_means_opt[f4,:],ribbon= 2 .*sqrt.(coeff_vars_opt[f4,:]),label=feature_names[f4])

plot!(p4,dates,coeff_m_s[f4,:],ribbon= 2 .*sqrt.(coeff_v_s[f4,:]),label=feature_names[f4]*" - Smoothed")

plot(p1,p2,p3,p4,size=(1000,1000),title = "Filtered VS. Smoothed",fmt=:png)