import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import torch

from scipy.special import roots_hermite

from scipy.stats import norm

import pyro

import pyro.distributions as dist

from matplotlib import pyplot

from torch.distributions import constraints

from pyro import poutine

from pyro.contrib.examples.finance import load_snp500

from pyro.infer import EnergyDistance, Predictive, SVI, Trace_ELBO

from pyro.infer.autoguide import AutoDiagonalNormal

from pyro.infer.reparam import DiscreteCosineReparam, StableReparam

from pyro.optim import ClippedAdam

from pyro.ops.tensor_utils import convolveVariational inference of latent state in state-space models

Core ideas

State space model

State transition: \[p(x_{t+1}|x_t)\]

Observation: \[p(y_t|x_t)\]

State trajectory distribution: \[p(x_{0:T})=p(x_0,x_1,x_2,...x_T)=p(x_0)p(x_1|x_0)p(x_2|x_1)...p(x_T|x_{T-1})\]

Parameter vector \(\theta\) for both state transition and observation distributions.

=> Find a posterior distribution

\[p(x_{0:T},\theta|y_{1:T})\]

Variational Inference

Approximate the posterior by

\[q(x_{0:T}, \theta)\]

such that the KL divergence between the posterior and the approximation is minimized.

\[q^*(x_{0:T},\theta)=\underset{q(x_{0:T},\theta)}{\operatorname{argmin}}KL(q(x_{0:T},\theta)||p(x_{0:T},\theta|y_{1:T}))\]

Here,

\[q(x_{0:T},\theta)=\prod_{t=0}^T q(x_t)\delta(\theta)\]

where \(\delta\) is the Dirac delta function. Roughly, with degenerate ‘uniform’ prior for \(\theta\), \(p(\theta)=C\) and independence between state and parameter prior, \[p(x_{0:T},\theta)=p(x_{0:T})p(\theta),\] this implies that we are looking for a MAP point estimate for \(\theta\). Now,

\[\begin{aligned} KL(q(x_{0:T},\theta)||p(x_{0:T},\theta|y_{1:T})) &=\int q(x_{0:T},\theta)\log\frac{q(x_{0:T},\theta)}{p(x_{0:T},\theta|y_{1:T})}d\theta dx_{0:T}\\ &=\int q(x_{0:T},\theta)\log\frac{q(x_{0:T},\theta)p(y_{1:T})}{p(x_{0:T},\theta,y_{1:T})}d\theta dx_{0:T}\\ &=\int q(x_{0:T},\theta)\log\frac{q(x_{0:T},\theta)}{p(x_{0:T},\theta,y_{1:T})}d\theta dx_{0:T}+\int q(x_{0:T},\theta)\log p(y_{1:T})d\theta dx_{0:T}\\ &=\int q(x_{0:T},\theta)\log\frac{q(x_{0:T},\theta)}{p(x_{0:T},\theta)p(y_{1:T}|x_{0:T},\theta)}d\theta dx_{0:T}+\log p(y_{1:T})\\ &=\int q(x_{0:T},\theta)\log\frac{q(x_{0:T},\theta)}{p(x_{0:T},\theta)}d\theta dx_{0:T}-\int q(x_{0:T},\theta)\log p(y_{1:T}|x_{0:T},\theta)d\theta dx_{0:T}+\log p(y_{1:T})\\ &=KL(q(x_{0:T},\theta)||p(x_{0:T},\theta))-\mathbb{E}_{q(x_{0:T},\theta)}[\log p(y_{1:T}|x_{0:T},\theta)]+\log p(y_{1:T})\\ &=KL(q(x_{0:T})\delta(\theta)||p(x_{0:T})p(\theta))-\mathbb{E}_{q(x_{0:T},\theta)}[\log p(y_{1:T}|x_{0:T},\theta)]+\text{const}\\ &=KL(q(x_{0:T})||p(x_{0:T}))+KL(\delta(\theta)||p(\theta))-\mathbb{E}_{q(x_{0:T},\theta)}[\log p(y_{1:T}|x_{0:T},\theta)]+\text{const}\\ &=KL(q(x_{0:T})||p(x_{0:T}))+\text{const}-\mathbb{E}_{q(x_{0:T},\theta)}[\log p(y_{1:T}|x_{0:T},\theta)]+\text{const}\\ \end{aligned}\]

Minimizing the KL divergence is equivalent to maximizing the ELBO (evidence lower bound) with respect to \(q(x_{0:T})\) and \(\theta\):

\[\text{ELBO}=\mathbb{E}_{q(x_{0:T},\theta)}[\log p(y_{1:T}|x_{0:T},\theta)]-KL(q(x_{0:T})||p(x_{0:T}))\]

Given our choice of \(q(x_{0:T},\theta)\), the ELBO can be simplified to

\[\text{ELBO}=\mathbb{E}_{q(x_{0:T})}[\log p(y_{1:T}|x_{0:T},\theta)]-KL(\prod_{t=0}^T q(x_t)||p(x_0)p(x_1|x_0)p(x_2|x_1)...p(x_T|x_{T-1}))\]

\[=\mathbb{E}_{q(x_{0:T})}[\log p(y_{1:T}|x_{0:T},\theta)]-KL(q(x_0)||p(x_0))-\sum_{t=1}^T\int q(x_t,x_{t-1}) \log\frac{q(x_t)}{p(x_t|x_{t-1})}dx_tdx_{t-1}\]

The last term can be written as follows:

\[\begin{aligned} \int q(x_t,x_{t-1}) \log\frac{q(x_t)}{p(x_t|x_{t-1})}dx_tdx_{t-1} &= \int q(x_t,x_{t-1})\log q(x_t)dx_tdx_{t-1}-\int q(x_t,x_{t-1})\log p(x_t|x_{t-1})dx_tdx_{t-1}\\ &= \int q(x_t)\log q(x_t)dx_t-\int q(x_t)q(x_{t-1})\log p(x_t|x_{t-1})dx_tdx_{t-1}\\ \end{aligned} \]

Now, we are stuck with \(\int q(x_t) q(x_{t-1})\log p(x_t|x_{t-1})dx_tdx_{t-1}\).

For specific cases of \(q(x_t)\), \(q(x_{t-1})\) and \(p(x_t|x_{t-1})\), we can solve.

Gaussian state-space model

Consider a Gaussian State transition and Gaussian variational distributions:

\[\begin{aligned} p(x_t|x_{t-1}) &= \mathcal{N}(x_t;\mu + Ax_{t-1},\Sigma)\\ q(x_t)&=\mathcal{N}(x_t;m_t,S_t) \forall t\\ \end{aligned}\]

This allows to simplify as follows:

\[\begin{aligned} \int q(x_t) q(x_{t-1})\log p(x_t|x_{t-1})dx_tdx_{t-1} &= \int q(x_t) \int q(x_{t-1})\log p(x_t|x_{t-1})dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\log \mathcal{N}(x_t;\mu + Ax_{t-1},\Sigma)dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|-\frac{1}{2}(x_t-\mu-Ax_{t-1})^T\Sigma^{-1}(x_t-\mu-Ax_{t-1})\right]dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|\right]-\frac{1}{2}\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\left[(x_t-\mu-Ax_{t-1})^T\Sigma^{-1}(x_t-\mu-Ax_{t-1})\right]dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|\right]-\frac{1}{2}\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\left[(x_t-\mu-Ax_{t-1})^T\Sigma^{-1}(x_t-\mu-Ax_{t-1})\right]dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|\right] \\ &\quad-\frac{1}{2}\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu + x_{t-1}^TA^T\Sigma^{-1}Ax_{t-1}-2x_t^T\Sigma^{-1} \mu - 2x_t^T\Sigma^{-1} Ax_{t-1} + 2\mu^T\Sigma^{-1}Ax_{t-1}\right]dx_{t-1}dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|\right] \\ &\quad-\frac{1}{2}\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu -2x_t^T\Sigma^{-1} \mu +\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})\left[x_{t-1}^TA^T\Sigma^{-1}Ax_{t-1} - 2x_t^T\Sigma^{-1} Ax_{t-1} + 2\mu^T\Sigma^{-1}Ax_{t-1}\right]dx_{t-1}\right]dx_t\\ &= \int \mathcal{N}(x_t;m_t,S_t) \left[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma|\right] \\ &\quad-\frac{1}{2}\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu -2x_t^T\Sigma^{-1} \mu - 2x_t^T\Sigma^{-1} Am_{t-1} + 2\mu^T\Sigma^{-1}Am_{t-1}+\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})x_{t-1}^TA^T\Sigma^{-1}Ax_{t-1}dx_{t-1}\right]dx_t\\ &= \int \mathcal{N}(x_t;m_t,S_t) \Bigg[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma| \\ &\quad-\frac{1}{2}\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu -2x_t^T\Sigma^{-1} \mu - 2x_t^T\Sigma^{-1} Am_{t-1} + 2\mu^T\Sigma^{-1}Am_{t-1}+\int \mathcal{N}(x_{t-1};m_{t-1},S_{t-1})x_{t-1}^TA^TL^{-1}(L^{-1})^TAx_{t-1}dx_{t-1}\right]\Bigg]dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \Bigg[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma| \\ &\quad-\frac{1}{2}\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu -2x_t^T\Sigma^{-1} \mu - 2x_t^T\Sigma^{-1} Am_{t-1} + 2\mu^T\Sigma^{-1}Am_{t-1}+\int \mathcal{N}(\tilde{x}_{t-1};(L^{-1})^T Am_{t-1},(L^{-1})^T AS_{t-1}A^T L^{-1})\tilde{x}_{t-1}^T \tilde{x}_{t-1}\right]\Bigg]dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \Bigg[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma| \\ &\quad-\frac{1}{2}\left[x_t^T\Sigma^{-1}x_t +\mu^T\Sigma^{-1}\mu -2x_t^T\Sigma^{-1} \mu - 2x_t^T\Sigma^{-1} Am_{t-1} + 2\mu^T\Sigma^{-1}Am_{t-1}+m_{t-1}^TA^TL^{-1}(L^{-1})^T Am_{t-1}+tr((L^{-1})^T AS_{t-1}A^T L^{-1})\right]\Bigg]dx_t \\ &= \int \mathcal{N}(x_t;m_t,S_t) \Bigg[-\frac{d}{2}\log(2\pi) -\frac{1}{2}\log|\Sigma| \\ &\quad-\frac{1}{2}\left[(x_t-\mu-Am_{t-1})^T\Sigma^{-1}(x_t-\mu-Am_{t-1})+tr((L^{-1})^T AS_{t-1}A^T L^{-1})\right]\Bigg]dx_t \\ &= \int\mathcal{N}(x_t;m_t,S_t) \log\mathcal{N}(x_t;\mu+Am_{t-1},\Sigma) dx_t -\frac{1}{2} tr((L^{-1})^T AS_{t-1}A^T L^{-1})\\ &= \int q(x_t) \log\mathcal{N}(x_t;\mu+Am_{t-1},\Sigma) dx_t - \frac{1}{2}tr((L^{-1})^T AS_{t-1}A^T L^{-1}) \end{aligned}\]

Plugging back in, we get

\[\begin{aligned} \int q(x_t)\log q(x_t)dx_t-\int q(x_t)q(x_{t-1})\log p(x_t|x_{t-1})dx_tdx_{t-1} &= \int q(x_t)\log q(x_t)dx_t- \int q(x_t) \log\mathcal{N}(x_t;\mu+Am_{t-1},\Sigma) dx_t + \frac{1}{2} tr((L^{-1})^T AS_{t-1}A^T L^{-1}) \\ &= KL(q(x_t)||\mathcal{N}(x_t;\mu+Am_{t-1},\Sigma)) + \frac{1}{2}tr((L^{-1})^T AS_{t-1}A^T L^{-1}) \end{aligned}\]

And thus, for the ELBO:

\[ELBO=\mathbb{E}_{q(x_{0:T})}[\log p(y_{1:T}|x_{0:T},\theta)]-KL(q(x_0)||p(x_0))-\sum_{t=1}^T KL(q(x_t)||\mathcal{N}(x_t;\mu+Am_{t-1},\Sigma)) - \frac{1}{2}tr((L^{-1})^T AS_{t-1}A^T L^{-1})\]

Therefore, we can propagate the variational Gaussian distribution \(q(x_{t-1})\) through \(p(x_t|x_{t-1})\) and marginalize the joint distribution. Then we can compute the KL divergence with \(q_{t}\) and add the correcting trace term.

The log-likelihood term can, depending on the either be computed analytically, approximated by sampling from \(q(x_{0:T})\) or by using Gaussian quadrature.

For a single dimensional, Gaussian state, quadrature is useful if the state-likelihood relation is non-Gaussian. E.g. for the stochastic volatility model, we have:

\[\begin{aligned} p(x_t|x_{t-1}) &= \mathcal{N}(x_t;x_{t-1},\sigma^2)\\ p(y_t|x_t) &= \mathcal{N}(y_t;\mu,\exp(x_t)) \end{aligned}\]

Rewrite the state-transition as follows: \[ \begin{aligned} p(x_t|x_{t-1}) &= \mathcal{N}(x_t;x_{t-1}),\sigma^2)\\ &= \mathcal{N}(x_t;0+1\cdot x_{t-1},\sigma^2)\\ \end{aligned} \]

With \(q(x_{t-1})=\mathcal{N}(x_{t-1};m_{t-1},s_{t-1}^2)\), the ELBO is then:

\[\begin{aligned} ELBO &= \mathbb{E}_{q(x_{0:T})}[\log p(y_{1:T}|x_{0:T},\theta)]-KL(q(x_0)||p(x_0))-\sum_{t=1}^T KL(q(x_t)||\mathcal{N}(x_t;m_{t-1},\sigma^2)) - \frac{1}{2}\frac{s_{t-1}^2}{\sigma^2} \\ \end{aligned} \]

class VariationalSVM:

def __init__(self, T_train, hermite_order=10):

self.T_train = T_train

self.mu_variational = torch.nn.Parameter(torch.randn(T_train+1)*0.1 - 3, requires_grad=True)

self.sigma_variational = torch.nn.Parameter(torch.randn(T_train+1)*0.1+np.log(0.1), requires_grad=True)

self.init_mu = torch.nn.Parameter(torch.tensor(0.0)-3, requires_grad=True)

self.init_sigma = torch.nn.Parameter(torch.tensor(np.log(0.1)), requires_grad=True)

self.obs_mu = torch.nn.Parameter(torch.tensor(0.0), requires_grad=True)

self.sv_sigma = torch.nn.Parameter(torch.tensor(np.log(0.1)), requires_grad=True)

self.hermite_roots = torch.tensor(roots_hermite(hermite_order)[0]).reshape(1,-1)

self.hermite_weights = torch.tensor(roots_hermite(hermite_order)[1]).reshape(1,-1)

def fit(self, y, epochs=3000, lr=0.01):

parameters = [self.mu_variational, self.sigma_variational, self.obs_mu, self.sv_sigma, self.init_mu, self.init_sigma]

y_torch = torch.tensor(y, dtype=torch.float32)

optimizer = torch.optim.RMSprop(parameters, lr=lr)

for epoch in range(epochs):

optimizer.zero_grad()

loss = -self.elbo(y_torch)

loss.backward()

optimizer.step()

if epoch % 300 == 0:

print(f"Epoch {epoch}: {loss}")

def elbo(self, y):

return (self.observation_likelihood(y) - self.state_kldiv() - self._kl_regularizer().sum())/ len(y)

def state_kldiv(self):

mu, sigma = self._forward_states(self.mu_variational[:-1])

obs_state_kldiv = torch.sum(self._gaussian_kl_divergence(self.mu_variational[1:], torch.exp(self.sigma_variational[1:]),mu, sigma))

init_state_kldiv = torch.sum(self._gaussian_kl_divergence(self.mu_variational[0], torch.exp(self.sigma_variational[0]), self.init_mu, torch.exp(self.init_sigma)))

return obs_state_kldiv + init_state_kldiv

def observation_likelihood(self, y):

mu, sigma = self.mu_variational[1:], torch.exp(self.sigma_variational[1:])

roots, weights = self.hermite_roots, self.hermite_weights

scaled_roots = mu.reshape(-1,1) + roots * sigma.reshape(-1,1) * torch.sqrt(torch.tensor(2.0))

dists = torch.distributions.Normal(self.obs_mu, torch.exp(scaled_roots)**0.5)

return 1.0 / np.sqrt(3.14) * torch.sum(weights * dists.log_prob(y.reshape(-1,1)), dim=1).sum()

def _gaussian_kl_divergence(self, mu_1, sigma_1, mu_2, sigma_2):

return torch.log(sigma_2) - torch.log(sigma_1) + (sigma_1**2 + (mu_1 - mu_2)**2) / (2*sigma_2**2) - 0.5

def _kl_regularizer(self):

return 0.5*torch.exp(self.sigma_variational[:-1])**2 / torch.exp(self.sv_sigma)**2

def _forward_states(self, x):

return x, torch.exp(self.sv_sigma) *torch.ones(x.shape)

Compare on Pyro Example for StochasticVolatility; replace Stable distribution by normal distribution.

df = load_snp500()

dates = df.Date.to_numpy()

x = torch.tensor(df["Close"]).float()

r = (x[1:] / x[:-1]).log()[-500:] #only last 500 observations for speed and plottabilitymodel = VariationalSVM(len(r))

model.fit(r, epochs=15000, lr=0.001)/var/folders/2d/hl2cr85d2pb2kfbmsng3267c0000gn/T/ipykernel_49291/2222375426.py:21: UserWarning: To copy construct from a tensor, it is recommended to use sourceTensor.clone().detach() or sourceTensor.clone().detach().requires_grad_(True), rather than torch.tensor(sourceTensor).

y_torch = torch.tensor(y, dtype=torch.float32)Epoch 0: 0.9661878450124246

Epoch 300: -0.25772427164926776

Epoch 600: -0.3492321266632049

Epoch 900: -0.490342730062777

Epoch 1200: -0.6414933041441354

Epoch 1500: -0.7935682951510592

Epoch 1800: -0.9452671538808363

Epoch 2100: -1.0963834713273448

Epoch 2400: -1.2466895941779013

Epoch 2700: -1.3956334504677272

Epoch 3000: -1.5422422327834961

Epoch 3300: -1.6860244318064324

Epoch 3600: -1.8277915821867003

Epoch 3900: -1.9672784887932344

Epoch 4200: -2.103803925148078

Epoch 4500: -2.2365100414646877

Epoch 4800: -2.3643368811629832

Epoch 5100: -2.486012826973618

Epoch 5400: -2.600165490082849

Epoch 5700: -2.705465957453146

Epoch 6000: -2.8008147693329484

Epoch 6300: -2.885494463111968

Epoch 6600: -2.9591203817006964

Epoch 6900: -3.0213672354173498

Epoch 7200: -3.072042840896504

Epoch 7500: -3.111557517459218

Epoch 7800: -3.1409610170015227

Epoch 8100: -3.1616046141000527

Epoch 8400: -3.175030289443991

Epoch 8700: -3.18284216999581

Epoch 9000: -3.1867202404968555

Epoch 9300: -3.1884403630441467

Epoch 9600: -3.189254063189258

Epoch 9900: -3.1897049427755735

Epoch 10200: -3.1900131335034554

Epoch 10500: -3.1902638271601513

Epoch 10800: -3.190479256186936

Epoch 11100: -3.1906677203082676

Epoch 11400: -3.1908336689280383

Epoch 11700: -3.1909784993302264

Epoch 12000: -3.1911046855451444

Epoch 12300: -3.1912133074056523

Epoch 12600: -3.1913101386746883

Epoch 12900: -3.191391568002003

Epoch 13200: -3.1914629692987635

Epoch 13500: -3.1915223461128126

Epoch 13800: -3.1915757805819176

Epoch 14100: -3.1916193830891646

Epoch 14400: -3.1916575531232443

Epoch 14700: -3.1916897356440823def pyro_model(data):

# Note we avoid plates because we'll later reparameterize along the time axis using

# DiscreteCosineReparam, breaking independence. This requires .unsqueeze()ing scalars.

h_0 = pyro.sample("h_0", dist.Normal(0, 1)).unsqueeze(-1)

sigma = pyro.sample("sigma", dist.LogNormal(0, 1)).unsqueeze(-1)

v = pyro.sample("v", dist.Normal(0, 1).expand(data.shape).to_event(1))

log_h = pyro.deterministic("log_h", h_0 + sigma * v.cumsum(dim=-1))

sqrt_h = log_h.mul(0.5).exp().clamp(min=1e-8, max=1e8)

# Observed log returns, assumed to be a Stable distribution scaled by sqrt(h).

r_loc = pyro.sample("r_loc", dist.Normal(0, 1e-2)).unsqueeze(-1)

pyro.sample("r", dist.Normal(r_loc, sqrt_h).to_event(1),

obs=data)

reparam_model = poutine.reparam(pyro_model, {"v": DiscreteCosineReparam()})

pyro.clear_param_store()

pyro.set_rng_seed(1234567890)

num_steps = 1001

optim = ClippedAdam({"lr": 0.05, "betas": (0.9, 0.99), "lrd": 0.1 ** (1 / num_steps)})

guide = AutoDiagonalNormal(reparam_model)

svi = SVI(reparam_model, guide, optim, Trace_ELBO())

losses = []

for step in range(num_steps):

loss = svi.step(r) / len(r)

losses.append(loss)

if step % 50 == 0:

median = guide.median()

print("step {} loss = {:0.6g}".format(step, loss))step 0 loss = 3.90561

step 50 loss = -1.45567

step 100 loss = -2.1139

step 150 loss = -2.66966

step 200 loss = -2.9662

step 250 loss = -2.8784

step 300 loss = -3.08116

step 350 loss = -2.98767

step 400 loss = -2.99272

step 450 loss = -3.07573

step 500 loss = -3.27141

step 550 loss = -3.23652

step 600 loss = -3.23926

step 650 loss = -3.20532

step 700 loss = -3.10074

step 750 loss = -3.25319

step 800 loss = -3.23684

step 850 loss = -3.27558

step 900 loss = -3.16651

step 950 loss = -3.27998

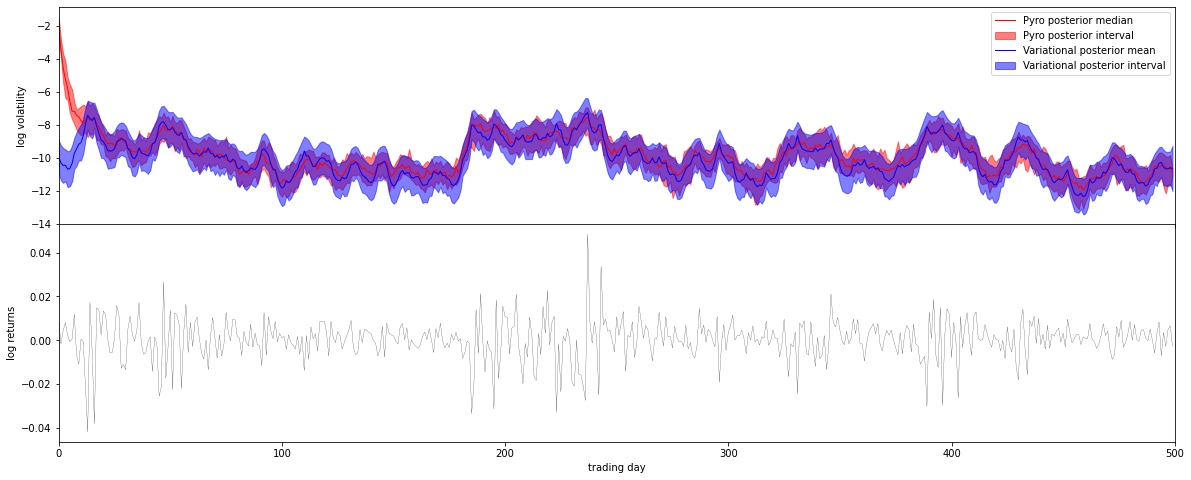

step 1000 loss = -3.26519vari_means = model.mu_variational.detach().numpy()

vari_stds = np.exp(model.sigma_variational.detach().numpy())

means = vari_means[1:]

lower_95 = norm.ppf(0.025, loc=vari_means[1:], scale=vari_stds[1:])

upper_95 = norm.ppf(0.975, loc=vari_means[1:], scale=vari_stds[1:])fig, axes = pyplot.subplots(2, figsize=(20, 8), sharex=True)

pyplot.subplots_adjust(hspace=0)

axes[1].plot(r, "k", lw=0.2)

axes[1].set_ylabel("log returns")

axes[1].set_xlim(0, len(r))

# We will pull out median log returns using the autoguide's .median() and poutines.

with torch.no_grad():

pred = Predictive(reparam_model, guide=guide, num_samples=20, parallel=True)(r)

log_h = pred["log_h"]

axes[0].plot(log_h.median(0).values, lw=1, color="red", label="Pyro posterior median")

axes[0].fill_between(torch.arange(len(log_h[0])),

log_h.kthvalue(2, dim=0).values,

log_h.kthvalue(18, dim=0).values,

color='red', alpha=0.5, label="Pyro posterior interval")

axes[0].plot(means, lw=1, color="blue", label="Variational posterior mean")

axes[0].fill_between(torch.arange(len(log_h[0])),

lower_95,

upper_95,

color='blue', alpha=0.5, label="Variational posterior interval")

axes[0].set_ylabel("log volatility")

axes[0].legend()

axes[1].set_xlabel("trading day");