Sarem Seitz

Home

Notebooks

About

Blog

Categories

All

(19)

Bayesian

(3)

Change Point Detection

(1)

Decision Trees

(4)

Gaussian Processes

(1)

Gradient Boosting

(2)

Julia

(1)

Kubernetes

(1)

Neural Networks

(1)

Tensorflow

(1)

Time Series

(13)

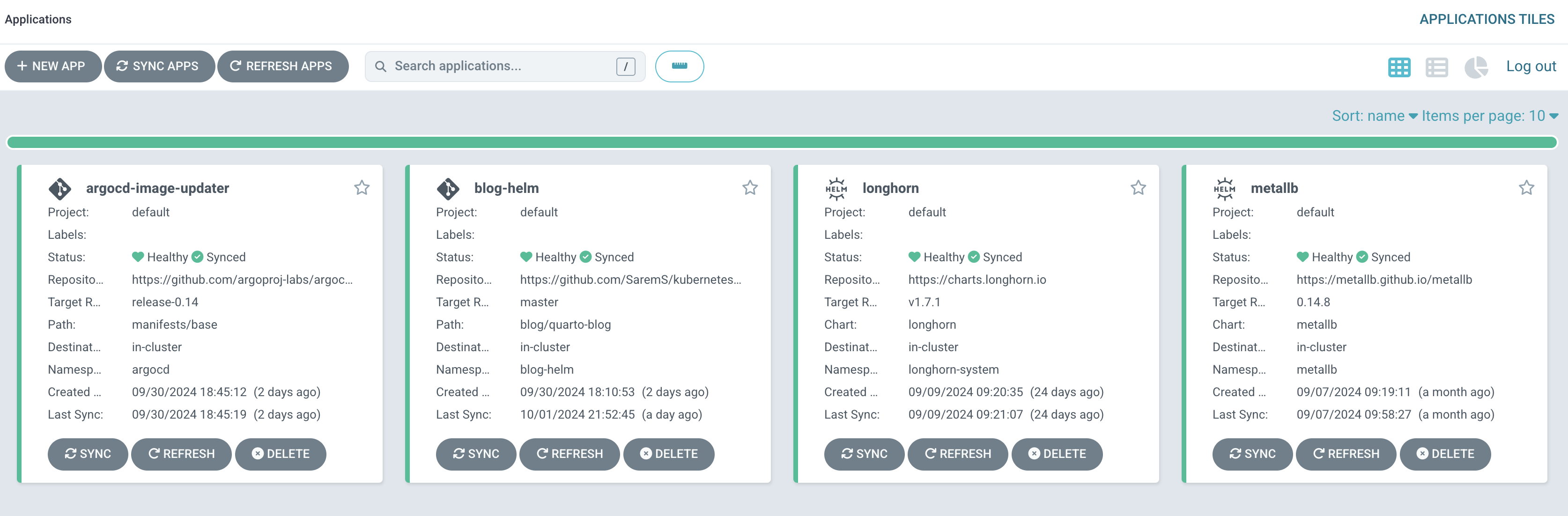

Hosting a static Blog on Bare-Metals Kubernetes - This could have been a GitHub pages site…

Kubernetes

In today’s tech landscape, Kubernetes has become synonymous with scalable and resilient application hosting. But what happens when you combine it with the relatively humble…

Oct 1, 2024

Sarem

With PyTorch, I can Gradient Boost anything

Decision Trees

Gradient Boosting

Gradient Boosting is a powerful machine learning technique that can be used for both regression and classification problems. Its fundamental idea is to combine weak, almost…

Jan 18, 2024

Sarem

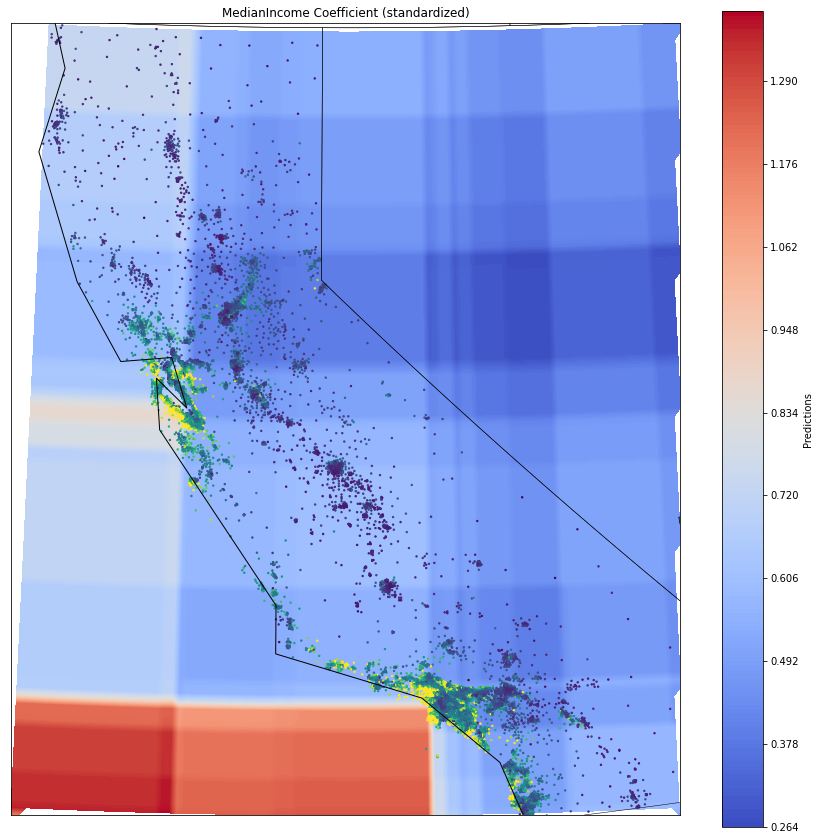

Varying Coefficient Boosting for geospatial and temporal data

Decision Trees

Gradient Boosting

Last time, amongst other ideas, we looked at how to implement Varying Coefficient Boosting in PyTorch. These types of models are quite useful, as they are considerably…

May 10, 2023

Sarem

Winning with Simple, not even Linear Time-Series Models

Time Series

Disclaimer: Title heavily inspired by this great talk.

May 10, 2023

Sarem

Varying Coefficient GARCH

Time Series

As you can probably tell by my other articles (for example here, here and here), I am a big fan of GARCH models. Forecasting conditional variance is arguably the best we can…

Jan 19, 2023

Sarem

When Point Forecasts Are Completely Useless

Time Series

In the last article, we discussed one advantage of probabilistic forecasts over point forecasts - namely, handling time-to-exceedance problems. In this post, we will examine…

Jan 1, 2023

Sarem

Why I prefer Probabilistic Forecasts - Hitting Time Probabilities

Time Series

Probabilistic forecasts are a more comprehensive way to predict future events compared to point forecasts. Probabilistic forecasts involve creating a model that predicts the…

Dec 6, 2022

Sarem

Random Forests and Boosting for ARCH-like volatility forecasts

Time Series

Decision Trees

In the last article, we discussed how Decision Trees and Random Forests can be used for forecasting. While mean and point forecasts are the most obvious applications, they…

Oct 7, 2022

Sarem

Forecasting with Decision Trees and Random Forests

Time Series

Decision Trees

Today, Deep Learning dominates many areas of modern machine learning. On the other hand, Decision Tree based models still shine particularly for tabular data. If you look up…

Sep 19, 2022

Sarem

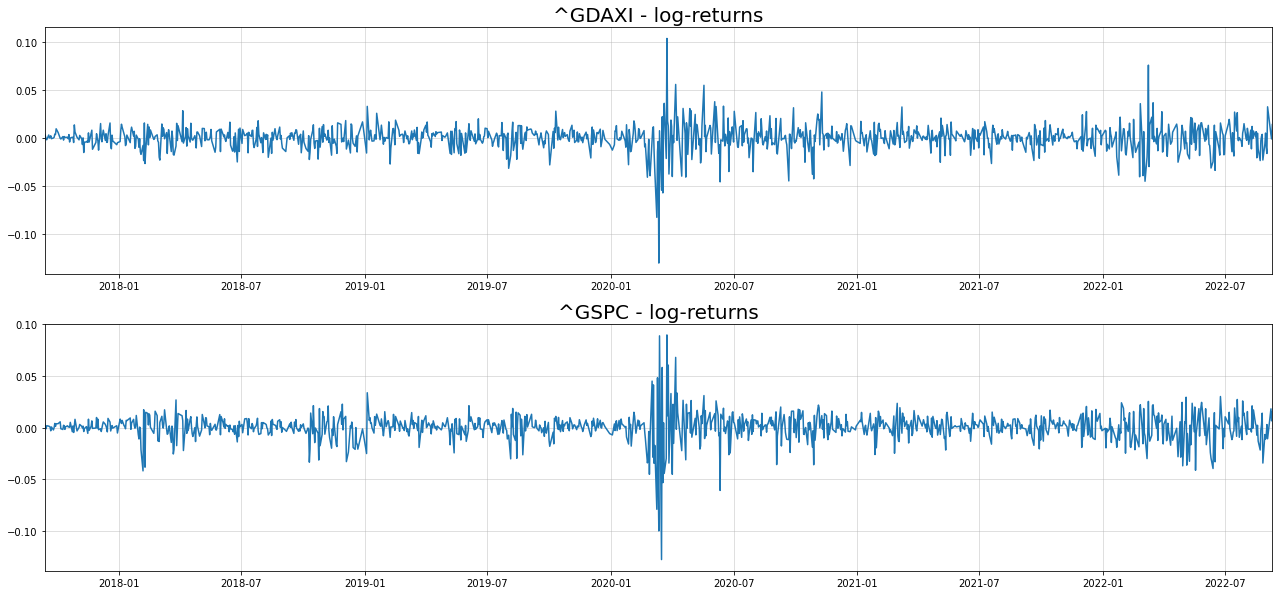

Multivariate GARCH with Python and Tensorflow

Time Series

Tensorflow

In an earlier article, we discussed how to replace the conditional Gaussian assumption in a traditional GARCH model. While such gimmicks are a good start, they are far from…

Sep 11, 2022

Sarem

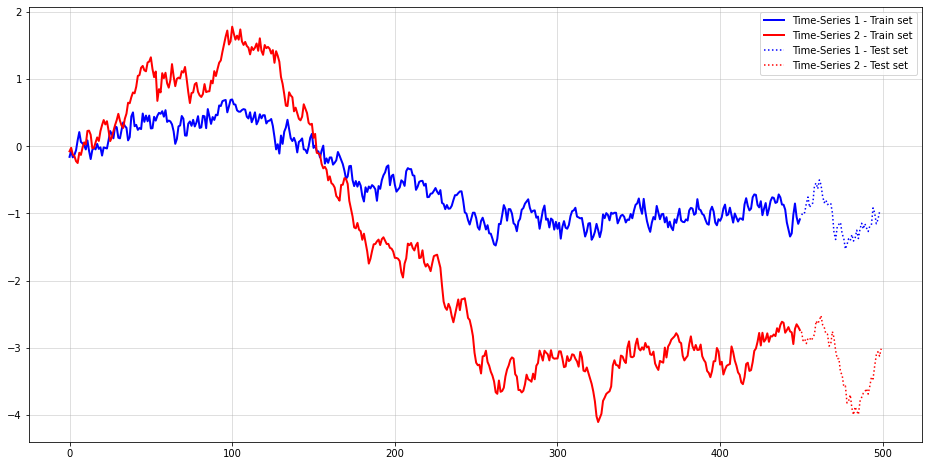

Cointegrated time-series and when differencing might be bad

Time Series

A standard method in the time-series analysis toolkit are difference transformations or

differencing

. Despite being dead simple, differencing can be quite powerful. In fact…

Aug 25, 2022

Sarem

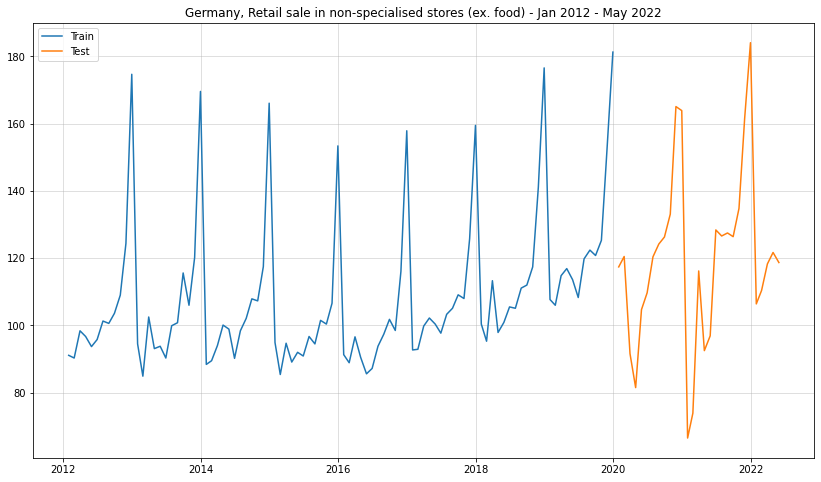

Facebook Prophet, Covid and why I don’t trust the Prophet

Time Series

Facebook Prophet is arguably one of the most widely known tools for time-series forecasting and related tasks. Ask any data scientist who works with time-series data if they…

Aug 8, 2022

Sarem

Probabilistic CUSUM for change point detection

Time Series

Change Point Detection

According to the famous principle of [Occam’s Razor], simpler models are more likely to be close to truth than complex ones. For change point detection problems - as in IoT…

Aug 4, 2022

Sarem

Multivariate, probabilistic time-series forecasting with LSTM and Gaussian Copula

Time Series

Neural Networks

As commonly known, LSTMs (Long short-term memory networks) are great for dealing with sequential data. One such example are multivariate time-series data. Here, LSTMs can…

Jun 30, 2022

Sarem

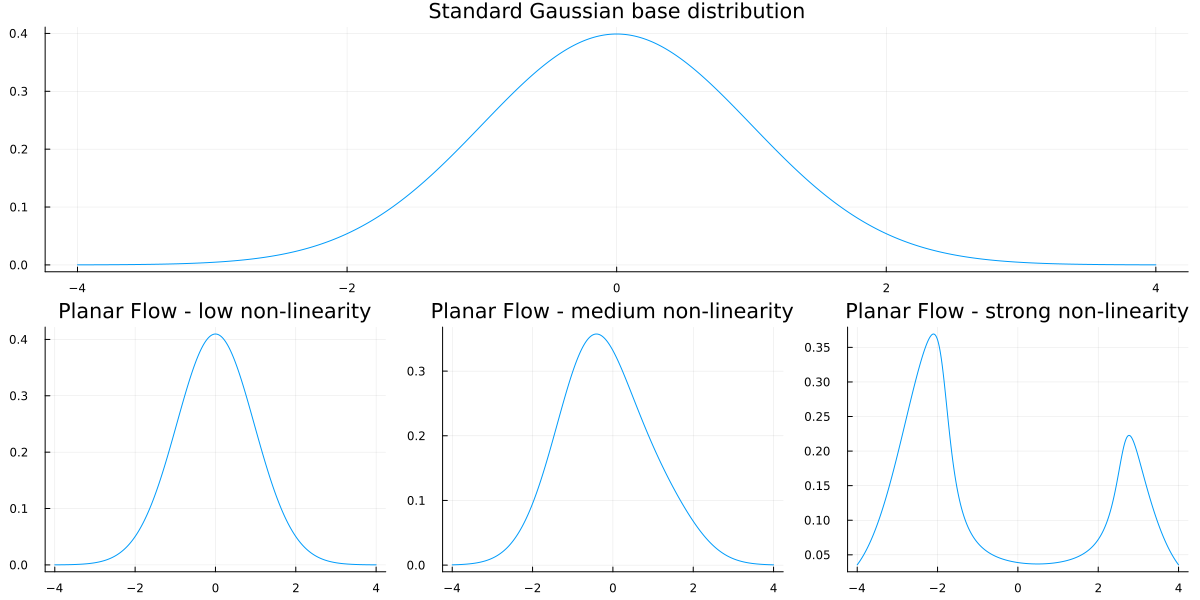

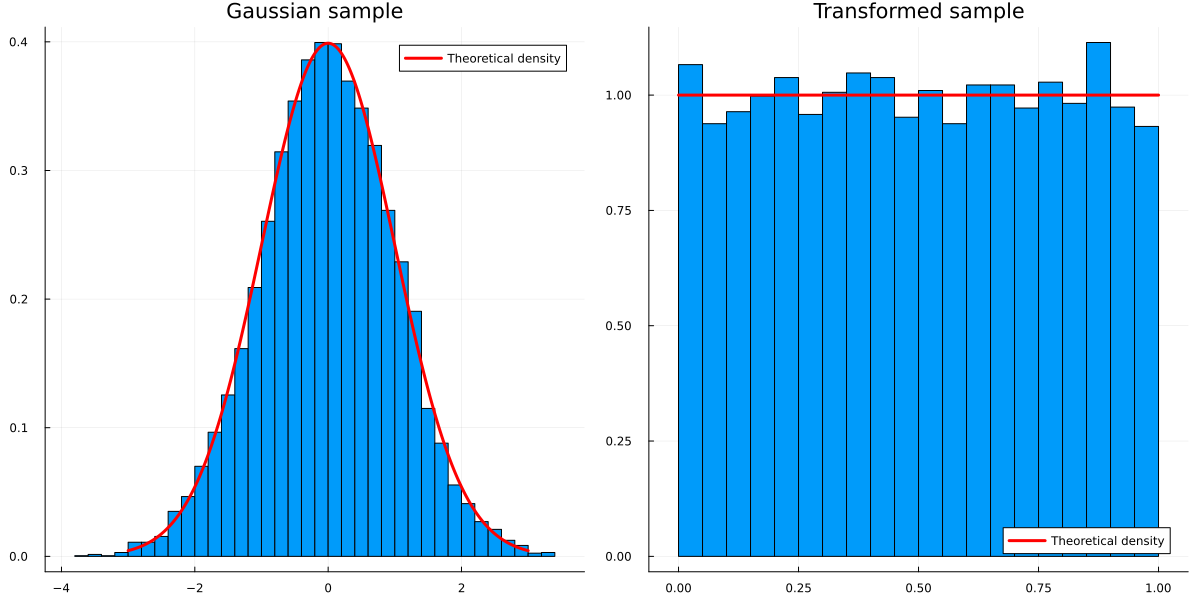

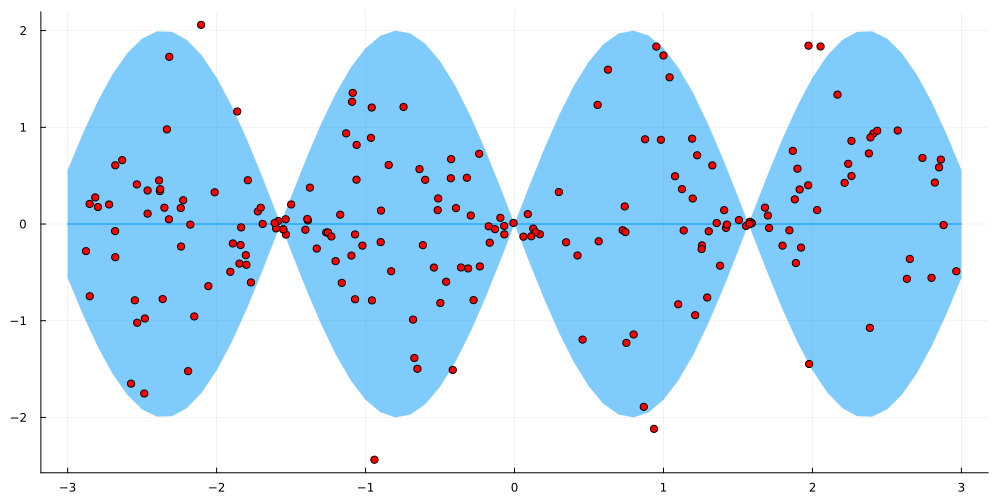

Let’s make GARCH more flexible with Normalizing Flows

Time Series

For financial time-series data, GARCH (Generalized AutoRegressive Conditional Heteroscedasticity) models play an important role. While forecasting mean returns is usually…

Jun 27, 2022

Sarem

ARMA forecasting for non-Gaussian time-series data using Copulas

Time Series

ARMA (AutoRegressive – Moving Average) models are arguably the most popular approach to time-series forecasting. Unfortunately, plain ARMA is made for Gaussian distributed…

Jun 17, 2022

Sarem

Bayesian Machine Learning and Julia are a match made in heaven

Bayesian

Julia

As I argued in an earlier article, Bayesian Machine Learning can be quite powerful. Building actual Bayesian models in Python, however, is sometimes a bit of a hassle. Most…

Mar 8, 2022

Sarem

When is Bayesian Machine Learning actually useful?

Bayesian

When it comes to Bayesian Machine Learning, you likely either love it or prefer to stay at a safe distance from anything Bayesian. Given that current state-of-the-art models…

Jan 22, 2022

Sarem

A Gaussian Process model for heteroscedasticity

Bayesian

Gaussian Processes

A common phenomenon when working on continuous regression problems is the non-constant residual variance, also known as heteroscedasticity. While heteroscedasticity is often…

Jun 28, 2021

Sarem

No matching items